Table of Content

On an average balance of $1,000, that’s $100 in interest charges each year. Beyond program-specific requirements, these special loans have some important drawbacks. Perhaps most importantly, they carryprivate mortgage insurance premiums until LTV reaches 78% (though you can formally request PMI removal at 80% LTV). In some cases, these annual premiums can exceed 1% of the total loan value – an extra $3,000 per year on a $300,000 loan, for instance. Historically, the ideal down payment has been at least 20% of the purchase price. In recent years, smaller down payments have come into vogue, thanks to looser underwriting requirements and growing acceptance among sellers.

NerdWallet strives to keep its information accurate and up to date. This information may be different than what you see when you visit a financial institution, service provider or specific product’s site. All financial products, shopping products and services are presented without warranty. When evaluating offers, please review the financial institution’s Terms and Conditions. If you find discrepancies with your credit score or information from your credit report, please contact TransUnion® directly.

Down Payment Assistance Programs

Most lenders offer some kind of DPA, but not all lenders have all types of programs available. To accelerate and simplify your debt payoff process, consider taking out a debt consolidation loanthrough SoFi that rolls all your disparate obligations into a single instrument. Many lenders make unsecured personal loans for just this purpose, so shop around for a lender whose products fit your credit profile and ability to repay. Start by doing some online research for down payment assistance programs available in your area.

If you're not planning on selling your current home, you won't have proceeds from the sale. That said, you can take out a home equity loan and put that money toward buying a second home. Finally, there are several ways you can use retirement funds for a down payment.

How to sell and buy a house at the same time

And the options that are available may come with higher costs. U.S. Department of Agriculture loans — Zero down payment loans are available for eligible applicants, but you’ll need to pay mortgage insurance to the USDA to use this loan program. The loans must be repaid over a certain period, such as 10 years. They make homeownership more attainable by spreading the down payment and closing costs over multiple years.

Some of these programs may offer down payment loans for qualifying borrowers. There are many programs and lenders that accept less than a 20% down payment during the purchase of a house. First, lenders will usually require borrowers to pay for insurance until they reach the 20% equity level.

What Will the Housing Market Look Like in 2023? A Buyer’s Guide

There are also plenty of first-time home buyer programs that let you put down as little as 3.5% or even 0%, and you can often qualify as long as you haven't owned a home in the last three years. The real cost of using your retirement accounts isn't the taxes or interest you pay but that those funds aren't growing for your retirement. The more aggressively you're invested, the greater that opportunity cost is likely to be. On the other hand, you have to weigh that against the value that owning a home can add as an asset that you can later sell or borrow against to help provide for your retirement. Federal Housing Administration loans — FHA loans are available to borrowers who are putting down as little as 3.5%, but they require mortgage insurance. Apply for a mortgage with a lender who is approved to work with the grant program.

The US Department of Housing and Urban Development offers a state-by-state list of programs. Sometimes local non-profit or government organizations can offer you a second mortgage on special terms to replace a down payment. For eligible servicemembers or family members, VA loans do not require a down payment. Money that you can spend on the down payment and closing costs. For instance, are you aware of the First-Time Homebuyer Act of 2021? While it’s still awaiting passage in Congress, if passed, the bill will provide a federal tax credit of up to $15,000 to first-time homebuyers.

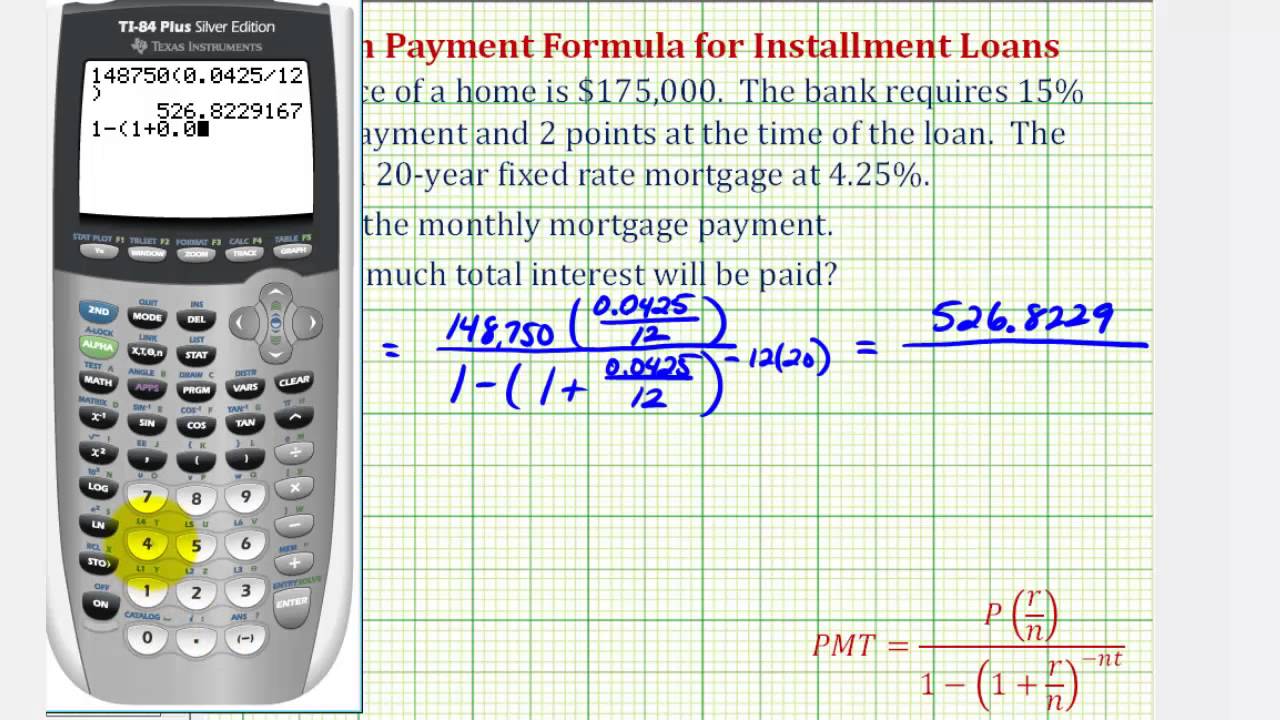

Let’s take a look at some loan options you may be considering. Let’s look at the different types of mortgage loans and their down payment requirements. If you want to become a homeowner, but you don’t have enough cash for a down payment, a state or local down payment assistance program might be able to help. The typical down payment on a mortgaged home in 2021 was 10-19% of the purchase price of the home. While 20% is the traditional down payment amount, 59% of buyers put down less than 20%, according to theZillow Group Consumer Housing Trends Report 2021. This down payment calculator provides customized information based on the information you provide.

That’s the minimum for a conventional or FHA loan, which are the most common mortgage types. There's no limit on how much you can use from gifts and loans for your down payment, but some loan programs require you to have a minimum borrower contribution. This means that you need to source a certain amount of your down payment from your own funds.

Quotes displayed in real-time or delayed by at least 15 minutes. The VA loan is a zero-down mortgage available to members of the U.S. military, veterans, and surviving spouses. Chase Bank serves nearly half of U.S. households with a broad range of products. For questions or concerns, please contact Chase customer service or let us know at Chase complaints and feedback.

However, you also have to consider the opportunity cost of taking that money out of your account, potentially for years . If you and your spouse both have IRAs, you can both withdraw up to $10,000, for a total of $20,000. Depending on the projected size of your down payment, that could be a sizable boost. And, on Roth IRAs held longer than five years, you can withdraw tax- and penalty-free contributions in excess of $10,000, though any withdrawn earnings are taxable at your normal rate. For instance, when you spend $3.69 on your morning latte, your debit card is charged $4, and the remaining $0.31 drops into your savings account. Multiply that by 50 or 100 transactions per month and you’ve got yourself a nice side pot.

For those looking to buy a home, PMI insurance adds to the monthly outlay of cash for payments. PMI payments are non-recoverable expenses that do not pay down the principal balance of your mortgage. On the other hand, coming up with 20% of a home's purchase price may take years to save up for, especially in hotter real estate markets. If you get a conventional loan, down payment assistance funds could save you a lot in mortgage insurance premiums over time.

Most people who don't have enough for the down payment accept private mortgage insurance as a necessary evil without first checking if they're eligible for assistance. For example, many banks have their own programs to help those looking to buy a home. Banks and other lenders often seek a down payment of 20% of the purchase price for the home. If you pay anything less, you'll need to buy private mortgage insurance . AlaskaAlaskans can find down payment assistance through the Affordable Housing Enhanced Loan program .

The MIP on an FHA Loan must be paid for the life of a loan if you put down less than 10-percent; some homeowners choose to refinance to remove this premium. Even if you don’t request cancellation, your servicer still must automatically terminate PMI on the date when your principal balance is scheduled to reach 78-percent of your home’s original value. For your PMI to be cancelled on this date, you must be current on your payments. Otherwise, PMI won’t be terminated until shortly after payments are brought up to date. You have the right to request that your loan service cancel PMI once you reach the date when the principal of your mortgage is scheduled to fall to 80-percent of the original value of your house.

No comments:

Post a Comment